Reports illustrate improvement of over $200 million against underfunded balance sheet obligations; projections include the expectation of a break-even result for the operating budget in the fiscal year ending June 30, 2018

Contextual Background

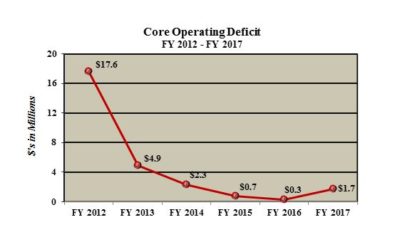

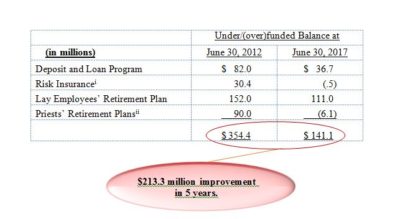

For the fiscal year ended June 30, 2012, the Archdiocese of Philadelphia disclosed a core operating deficit of $17.6 million as well as underfunded balance sheet obligations totaling $354.4 million.

Since that time, results have improved significantly as reflected in the graph and the table presented below. The core operating deficit for the fiscal year ended June 30, 2017 was approximately $1.7 million. While that result is higher than our recent trend, it is consistent with our expectation and we have taken steps to ensure a break-even result for the fiscal year ended June 30, 2018.

In addition, as of the fiscal year ended June 30, 2017, the Archdiocese has reduced its underfunded balance sheet obligations by $213.3 million over the course of five years.

Analysis of Fiscal Year Ended June 30, 2017

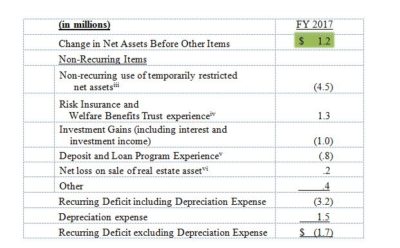

The analysis below presents the “Change in Net Assets Before Other Items” for the year ended June 30, 2017. This amount (i.e. the $1.2 million surplus shaded below) can be found in the Statement of Activities and Changes in Net Assets under the caption “Change in Net Assets Before Other Items” in the “Unrestricted” column (the actual amount is $1,230,176 which has been rounded to $1.2 million in the presentation below). We believe that the analysis presented below provides a meaningful disclosure of results after adjusting for the impact of items that are non-recurring in nature.

The “Recurring Deficit excluding Depreciation Expense” caption above represents what we refer to as our “core” (excludes items of a non-recurring nature and depreciation) run rate deficit.

While the FY 2017 result reflects a larger annual deficit than we have experienced recently it is consistent with our expectation and the deficit budgeted for the fiscal year. In the narrative that we published in connection with the disclosure of our results for the fiscal year ended June 30, 2016 we noted then, when referencing the $300,000 core run rate deficit incurred, that we believed our “sustainable run rate deficit is still higher and we will need to take actions in the near term in order to achieve a sustainable break-even or better result.” During the fiscal year just ended we did take specific actions to deliver a break-even result in the near term. Specifically we have fully funded the priests’ retirement plans, allowing us to reduce amounts charged for these benefits, and we have also increased the assessment charged to parishes. These actions should allow us to achieve break-even operating results in the near term and we have budgeted accordingly for our fiscal year ending June 30, 2018.

Discussion of Other Significant Matters

In connection with our recent financial disclosures we have provided specific commentary regarding certain balance sheet obligations. As of June 30, 2017 the following balance sheet obligations remain underfunded:

- Deposit and Loan Program Trust

- Lay Employees’ Retirement Plan

Please find an update as of June 30, 2017 for each of these obligations below.

Deposit and Loan Program [vii]

Included in the financial statements for the Office for Financial Services are all assets and liabilities of the Archdiocese of Philadelphia Deposit and Loan Program Trust Fund (“Deposit and Loan Program Trust” or “D&L”). The Deposit and Loan Program Trust is a separate legal entity that provides a deposit and loan program for the benefit of parishes to assure continuation of the ecclesial goals of the Archdiocese and the parishes. If a parish deposits funds in the Deposit and Loan Program Trust, it receives a competitive interest rate. In turn, these funds are loaned to other parishes for construction and other projects.

During the year ended June 30, 2012, the Archdiocese executed a promissory note to the Deposit and Loan Program Trust in the amount of $82 million, which represented the excess of deposits over assets as of June 30, 2012. The promissory note is collateralized by specific pledged real estate assets which are documented in the note. As pledged properties are sold or monetized, net proceeds from these collateral transactions will be deposited into the Deposit and Loan Program Trust, in accordance with the provisions of the promissory note. In the event a transaction generates in excess of $20 million in net proceeds, the Archdiocese has discretion regarding alternative uses for the excess so long as remaining pledged assets are at least equal to the then outstanding principal amount owed.

As of June 30, 2017 the underfunded obligation (i.e. the excess of deposits over assets) in the Deposit and Loan Program Trust was as follows:

As of June 30, 2017 the balance outstanding on the promissory note was $41,689,805, which is greater than the underfunded obligation noted above.

The following properties are pledged as part of the promissory note:

- Sproul Road property in Marple Township (Delaware County)

- Manor Road Property (Chester County)

We estimate that the value associated with the properties noted above and other pledged properties will be sufficient to resolve the remaining underfunded obligation in the Deposit and Loan Program Trust.

Lay Employees’ Retirement Plan

The Lay Employees’ Retirement Plan (LERP) is considered a multiemployer plan for financial reporting purposes. As such, the assets and actuarially determined liabilities for this plan are not included in the OFS financial statements. The Archdiocese froze this defined benefit pension plan effective June 30, 2014.

While not a direct liability of OFS the amount by which the plan liability exceeds plan assets is a liability of the Archdiocese. The preliminary estimate of the actuarially determined liability for this plan as of June 30, 2017 was $622 million.

When the estimated liability is compared to plan assets available for benefits as of June 30, 2017 (approximately $511 million), the plan’s shortfall is approximately $111 million. The funded status of the LERP as of June 30, 2017 has improved to 82.1%, versus 70.7% as of June 30, 2016.

Looking Forward

The core operating deficit has been stabilized significantly since FY 2012’s deficit of $17.6 million. As noted earlier we have taken steps to improve our operating results in the near term and we expect to achieve a break-even result in our fiscal year ended June 30, 2018.

As noted earlier, we estimate that the value associated with properties pledged for the Deposit and Loan Program promissory note is sufficient to resolve the remaining underfunded obligation once those properties are sold.

Going forward our remaining balance sheet issue will be the underfunded Lay Employees’ Retirement Plan. We have taken the following significant steps to address the Lay Employees’ Retirement Plan:

- froze the plan effective June 30, 2014;

- completed more than $100 million of lump sum distributions in calendar year 2015 to eligible participants at a rate equivalent to 85.1% of the present value of their normal retirement benefit;

- made an unplanned contribution of $7.5 million during the fiscal year ended June 30, 2016 and an unplanned contribution of $30 million during the fiscal year ended June 30, 2017;

- and increased the funding rate to 5.9% from 4% of “pension eligible payroll” effective July 1, 2016. Based on the most recently completed actuarial valuation for the plan (as of July 1, 2017), if we maintain a funding rate of 5.9%, and all other actuarial assumptions are achieved, the plan should be fully funded in approximately 15 years.

Additional Financial Statements for the Fiscal Year Ended June 30, 2017

The audited financial statements for OFS do not include financial results for the Office of Catholic Education, Catholic Healthcare Services, Catholic Social Services, Saint Charles Borromeo Seminary, Catholic Charities Appeal or the Heritage of Faith—Vision of Hope Capital Campaign as all are separate entities. Audited financial statements for these entities will be published in the coming weeks.

Additionally, none of the reports released by the Archdiocese include financial statements for individual parishes. All parishes are independent and autonomous entities.

# # #

Editor’s Note:

A complete copy of the audited financial statements for the Office for Financial Services for the fiscal years ended June 30, 2017 and June 30, 2016 can be found at www.CatholicPhilly.com.

Endnotes

[i] Risk Insurance Trust assets ($38.2M) exceeded liabilities ($37.7M) by $.5M at June 30, 2017.

[ii] Priests’ retirement plans’ assets ($106.8M) exceeded liabilities ($100.7M) by $6.1M at June 30, 2017.

[iii] Represents use of $4.5M of temporarily restricted net assets to relocate the historical archives of the Archdiocese of Philadelphia to the newly established Catholic Historical Research Center of the Archdiocese of Philadelphia. The funds for this project were raised in connection with the Catholic Life 2000 capital campaign.

[iv] The experience of the Risk Insurance and Welfare Benefits Trust should be considered separately and treated as non-recurring. The assets in this trust are not available for general operating needs.

[v] The experience of the Deposit and Loan Program should be considered separately and treated as non-recurring. The assets in this program are not available for general operating needs.

[vi] The amount represents the net loss resulting from the sale of an Archdiocesan property.

[vii] As disclosed in the audited financial statements, effective February 17, 2017 the trustees of the D&L instituted a moratorium on accepting deposits, opening new accounts and making new loans under the program. Additionally, the trustees implemented a distribution from the D&L of parish cemetery perpetual care funds and endowment funds so that these balances could be more appropriately invested. Cash distributions, equal to 20% of depositor balances, were also made to each depositor.

Contact:

Contact: Kenneth A. Gavin

Chief Communications Officer

215-587-3747 (office)